Recently, I started documenting some of the major changes going on in my life (such as the wedding). At the end of this month, a long term goal has finally come to fruition; Allison and I are making settlement on a house. I wanted to write something to document our experiences and to offer some advice to those who may be looking. Like a snowflake, this is my unique experience and everyone’s stories will be different, but there I am sure you can pick up some good points.

Section One: The Housing Market

I started looking at houses in 2004. The housing market was experiencing tremendous growth and I started to get a little concerned that I would be priced out and not able to afford a house if I waited (like all the other buyers out there). I was raised on the principle that renting was throwing money away, so that wasn’t an option. By the middle of 2004, housing prices had almost doubled from just 2002. During this time I owned a computer repair shop and kept a full time job doing IT work for an insurance company. The driving between my house, my store, and my day job was starting to take its toll and I wanted a place closer to the jobs.

I started looking at houses in 2004. The housing market was experiencing tremendous growth and I started to get a little concerned that I would be priced out and not able to afford a house if I waited (like all the other buyers out there). I was raised on the principle that renting was throwing money away, so that wasn’t an option. By the middle of 2004, housing prices had almost doubled from just 2002. During this time I owned a computer repair shop and kept a full time job doing IT work for an insurance company. The driving between my house, my store, and my day job was starting to take its toll and I wanted a place closer to the jobs.

I was part of a business referral group and the president of the group happened to be a realtor. I figured it would be good to do business with him because it might give “Computer Joey” (my shop) a boost too. The gentlemen showed me a few houses, but as a whole, he was very difficult to get in contact with. I would give him a price range and he would come back with houses 30-60k higher saying there was nothing in the area, but sadly for this realtor, I had something called the internet and could look up almost the same information he had access to. This is where I started to come under the impression that real-estate agents are shady people. LET ME REPEAT: NEVER TRUST A REALTOR (Brad is exempt from this comment). Only you can look out for your best interests, don’t expect to get unbiased advice as a general rule.

I shifted through a few realtors, focusing on Berlin, NJ which was where my store was located. As each month passed, the prices of the homes kept increasing as did my anxiety. As I walked into each home, I would say to myself “this house isn’t worth anywhere near the asking price, not by a long shot”. The next day it would be gone, sold for the asking price, and I was left scratching my head.

In 2005, two major changes happened, I started getting serious with Allison and my buddy Brad from work became my realtor. Brad is a hilarious, great guy, but if I could do it all over again, I wouldn’t mix friends and business like that. Brad showed me homes for the next 30 months: I kept changing my mind about locations, housing styles, price ranges and I know he got sick and tired of dealing with me and I was frustrated because I wanted my friend to make some money.

In the (almost) three years that I looked for houses, I focused on Berlin, Marlton, Collingswood, Haddon Heights, Haddon Township , Sewell, Pitman, Swedesboro, Mullica Hill, and Mantua township (this is all South Jersey). My price range has gone from 150,000 to 350,000 and back down. I looked a single homes, duplexes (and triplexes), condos and townhomes. To say it was like a full time job, would be an understatement.

Getting back to the market… As houses became more overpriced, I started hearing more about people doing creative financing, and I am not going to sugarcoat it, Brad mentioned it a few times, but something felt wrong about it. To make this long story short, regardless of the neighborhood, I was having a hard time rationalizing paying 250,000 for a 1300 square foot house with one bathroom, a kitchen that needed to be ripped out, the basement not being livable space and people telling me it was a good deal. But now I started to understand why these houses were going, it was easy for people to borrow money, and they were under the assumption the loan was cheap.

Section Two: Advice

There are a few simple things I learned in my housing travels:

1. If the house is empty and looks nice inside, it is probably a flip. This means the people are going to want the highest price (especially in this market because they bought it high) and the work is going to be done on the cheap

2. On the reverse, empty houses that look a bit older and a great find because it probably means it is an estate sale and the family doesn’t want the nightmare of haggling with people (that is the situation we found with our house)

3. Never be afraid to throw a low ball offer out there. Let me repeat: DON’T BE AFRAID TO LOWBALL. Brad always had a tough time with my low bids and hesitated and tried to talk me out of it. Fuck that. If they don’t want to give it to you, just walk away.

4. Don’t get stuck. There are times I found myself bidding on houses, starting with a low bid and having a price in my head where I would walk, but the bidding gets into your blood and you want to win, so you end up going higher than you wanted to. Don’t do this.

5. Right now, if you are buying (and if you don’t have a house to sell) you are in the drivers’ seat. There are no buyers right now, take advantage of it and put the screws to these sellers.

6. I find Yahoo Real Estate engine to be the best, it gives the information in a nice format, the pictures are better, and you can set up reports that will automatically alert you when something hits the market in your range. Yahoo also gives the address of the property…

7. Which leads me to Google Earth. Zoom in on the property you are looking at. See how close train tracks are, dumps, swamps, etc.

Section Three: Why are there no buyers?

If you have been living under a rock the last year and didn’t read about the mortgage and lending crisis this country is currently experiencing, let me break it down for you:

1. In 2003, mortgage companies (and some banks) started finding creative ways to get people who could not afford to buy homes a way to get into the “home of their dreams”. ARMs, interest only loans, no money down incentives got people out of apartments and created a booming seller market.

2. The interest rate dropped below 6%

3. These creative loan programs offered reduced payments the first few years of the loan and then the house payment would balloon up or you would be in a loan where you never pay against the principle of the house and you hope the value of your home goes up (which is the only way to build equity).

4. The lending companies were getting huge loans from the banks, cutting them up, selling them in chucks, and then another company would do the same thing (and so on). This practice made the loan requirements disappear. It didn’t matter what your lot in life was, you could find somebody to sell you a mortgage.

5. People who could not afford a home, now had funding and went crazy. Multiple people bidding on the same home, driving the price of the home up or in a lot of cases people just going in and offering MORE than asking just to avoid the bidding war.

6. Home owners not moving suddenly found themselves sitting on tiny gold mines as their house doubled and tripled in value. Depressed areas were even seeing upswing as people who unable to buy in the better areas brought money into the lower ones. Home owners started to view their houses as bank accounts and pulled money out to buy stuff or pay off dept.

7. Prospectors took the cheap loans and started snapping up houses and flipping them (making it even harder to find a good deal)

8. Eventually, when the ARM loans matured to full price, the home prices became so high that people of means couldn’t afford modest homes – the market started to slow down, the bubble burst.

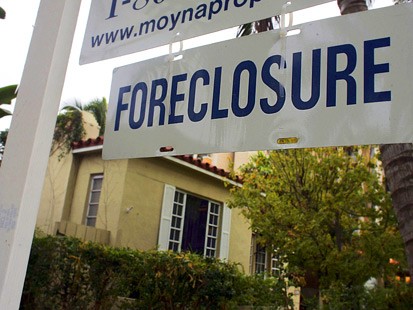

9. Mortgaging companies are going out of business. Standards and limits are finally coming back, knocking unqualified buyers out of the running.

10. People can’t afford their houses. As houses depreciate in value, and monthly payments go up for the owners, getting out of the house with a profit becomes much harder. Factor in fact 9 and there is nobody around to buy that house even at a loss.

Commentary: I have absolutely no sympathy for people losing their homes at the moment. I know that might sound mean, but it was because of them and their foolish purchasing habits that got EVERYONE into this mess. People who own homes pulled money out to remodel their houses or worse, to buy crap. Our fellow buyers got the house but soon realized they didn’t even have money for furniture. Now foreclosure rates are skyrocketing and people are getting tossed out on their asses.

Commentary: I have absolutely no sympathy for people losing their homes at the moment. I know that might sound mean, but it was because of them and their foolish purchasing habits that got EVERYONE into this mess. People who own homes pulled money out to remodel their houses or worse, to buy crap. Our fellow buyers got the house but soon realized they didn’t even have money for furniture. Now foreclosure rates are skyrocketing and people are getting tossed out on their asses.

I read an article on MSNBC about a woman who lost everything. She bought a condo in Vegas for 400,000. She was taking home $2,000 cash per month. Who the hell gave this woman the loan and how did she think she was going to afford. This isn’t hard math… know what your limit is, and then go under it (Your mortgage should not be more than 28% of your gross income).

Section 4: Carpe Diem

Right now is an excellent time to buy a house if you are a first time home buyer. All of those creative mortgages are biting people in the ass and they can’t afford to live in their homes. Make their mistake your advantage. Remember, people are going to want to get the highest price (as always) because that is going to be less debt they are in, screw that… every month they pay, is money they loose.

Another thing to factor in is what is what the rest of the neighborhood selling for. This numbers might be off if the houses sold last year as opposed to the last 6 months. In our situation (we bought a townhome), there were 6 houses for sale that were almost exactly the same, we pitted all of the sellers against each other. In the end it worked out great for us: the perfect storm of buying opportunities converged and got us into a great house and at an excellent price.

You can do it too, don’t be afraid, and remember that you are always in the divers seat regardless of the market.

Good luck!